Crude Truths and ‘Strait’ Faces

Published on April 23rd, 2026

In our analyses, we regularly examine current movements, identify possible influencing factors and assess the general market situation. However, these are not recommendations, but merely opinions and food for thought.

Find out more about Pretiorates.com

Dear readers,

Before we get to the new thoughts, check out the AI video from our last edition:

Pretiorates’ Thoughts — Climbing While the World Wobbles

Please watch and give it a like! Or even better: subscribe to our AI channel!

Pretiorates’ Thoughts – Crude Truths and ‘Strait’ Faces

In the Strait of Hormuz, nothing is off the table. The world has been informed that the U.S. military has blocked the strait. At the same time, we read that the Iranian Revolutionary Guards have blocked it. It is currently difficult to clearly distinguish who has a monopoly on the truth and what belongs more in the realm of propaganda.

Our baseline scenario remains unchanged: the war with Iran is likely to persist for some time. At the same time, neither Iran, the U.S., nor China has a serious interest in exports through the Strait of Hormuz remaining blocked for much longer. This is not just about energy sources like oil and gas, but also about helium for the chip industry, sulfuric acid for mining, and precursors for fertilizers, on which U.S. farmers also depend.

Both sides are therefore likely to have a growing interest in reaching an agreement soon. While the U.S. is increasingly positioning itself as a global energy powerhouse, the conflict is politically unpalatable at home: High gas prices are about as popular in the U.S. as rain at a barbecue, and the course of the Iran conflict so far could cost U.S. President Trump the midterm elections in November. Iran, too, is unlikely to benefit in the long run, even if transit fees were to be imposed in the future. An ‘Aya-Toll-Ah’ regime would likely isolate the country even further within the Islamic world of neighboring states and exporters.

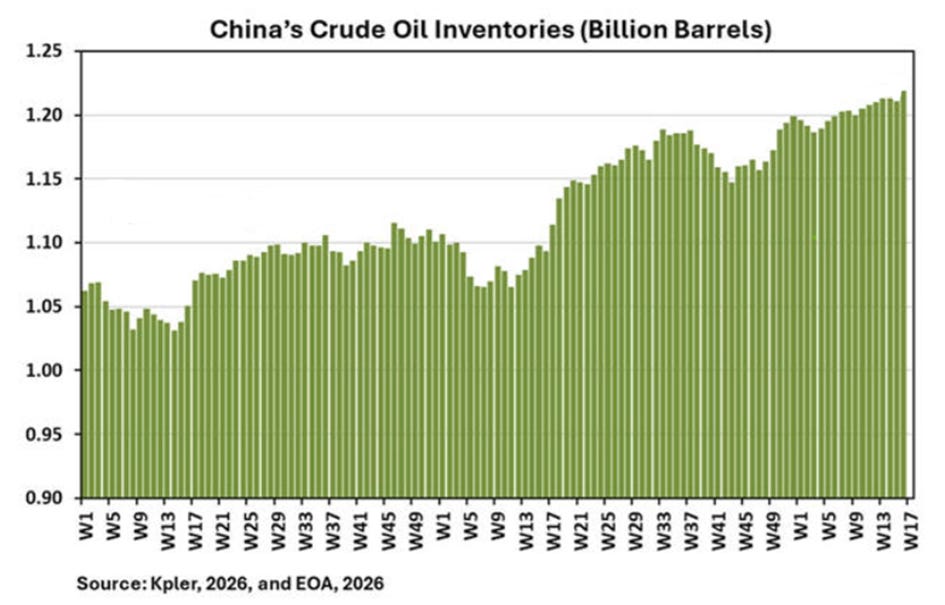

The U.S. blockade could lead, within 15 days at the latest, to the Iranian state running out of liquidity—funds that have so far come from the daily sale of around 2 million barrels of oil to China. And China, for its part, has a strong interest in ensuring the blockade does not continue any longer—even though oil reserves were expanded to record levels by last week. These stocks are unlikely to rise much higher: the last tanker that was able to set sail for China before the outbreak of war reached the country about ten days ago.

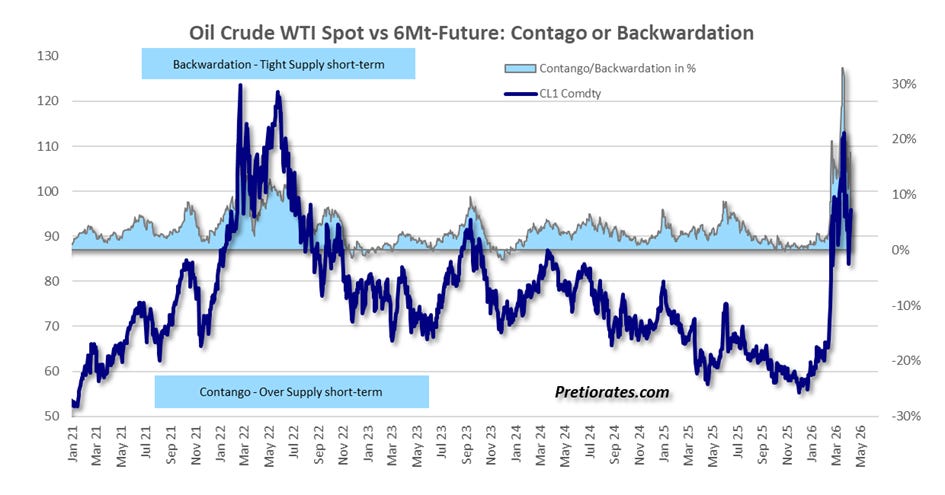

The oil market itself also continues to signal that the situation should calm down soon. While the spot price has risen back to near $100 per barrel amid the general nervousness surrounding ceasefires, the six-month futures contract is currently trading no less than 17% lower. At its peak earlier this month, the spread was even well over 30%. Normally, the futures contract should trade above the spot price—storage and financing costs are not free. The market’s message is therefore all the clearer: perhaps not the war itself, but the market assumes that exports through the Strait of Hormuz should be possible again in six months.

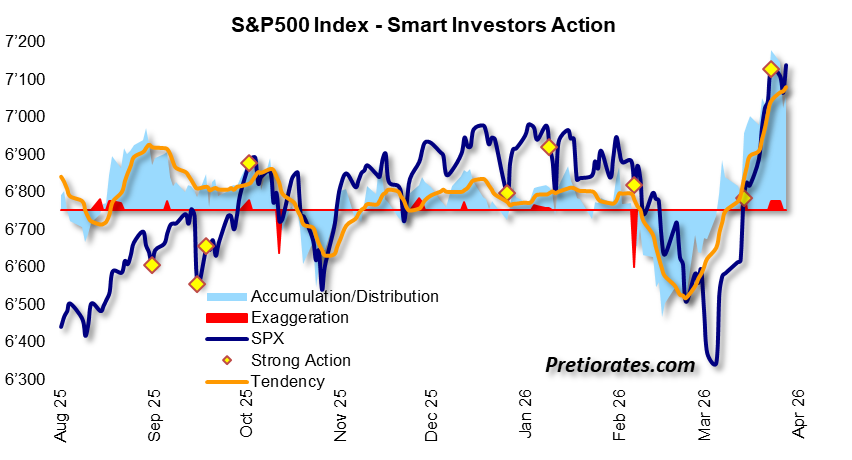

Meanwhile, on Wall Street, accumulation is taking place as rarely before. While we have braced ourselves for rising stock prices over the past three weeks, the extent of the rally—likely a mix of excessive fear, underinvestment, and short covering—is nonetheless surprising. The light blue area in the positive zone illustrates the scale of this buying frenzy. Recently, however, it has been accompanied by ‘Strong Action’ (the yellow dot) and a slight ‘Exaggeration’ (the red area). This combination often signals a trend reversal. It would therefore come as no surprise if we see increased profit-taking over the next one to two weeks.

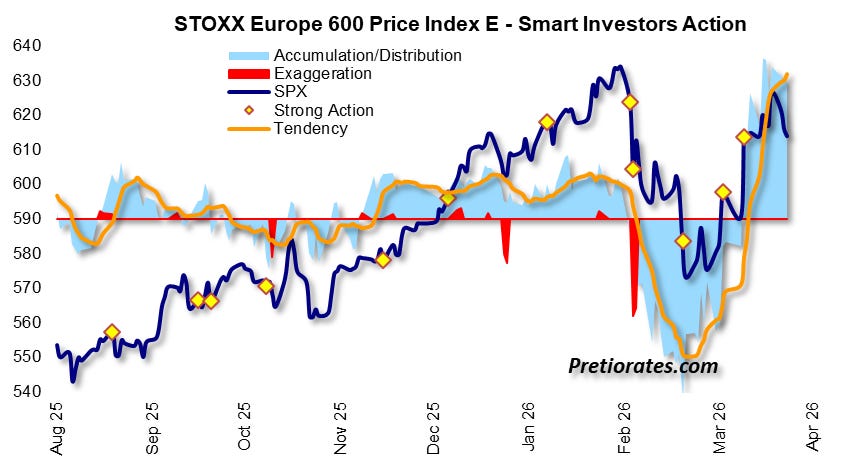

In Europe, too, the stock markets have recovered. Nevertheless, it was not enough to reach a new all-time high. And this despite the fact that accumulation has reached a distinctly aggressive level here as well. This is not entirely surprising: While China can tap into additional energy suppliers besides Venezuela and Iran, the alternatives for Europe are becoming fewer rather than more.

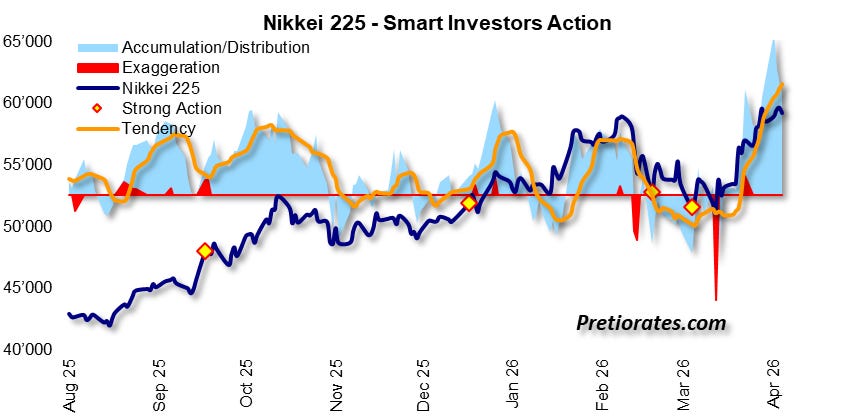

Even the Japanese Nikkei recently surpassed the 60,000-point mark for the first time in its history. A key contributor to this was, of course, the persistently weak Japanese currency, which is bringing higher sales prices into exporters’ coffers.

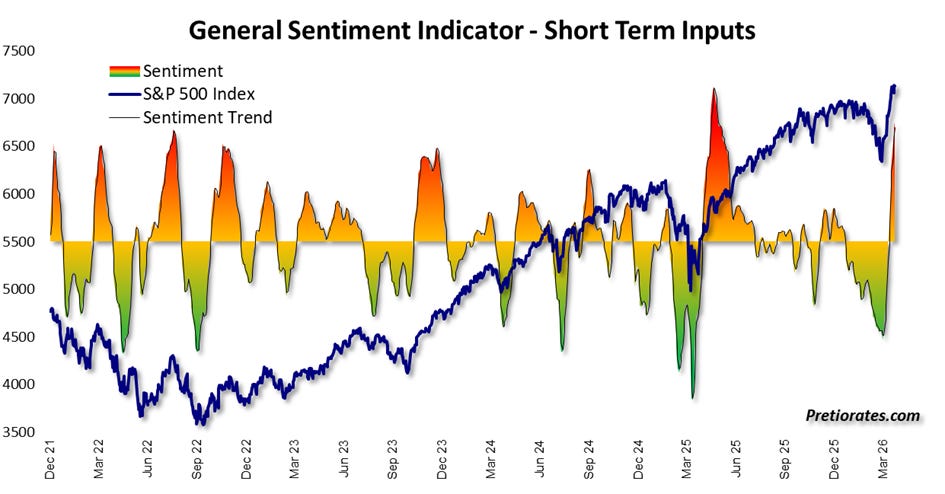

Following the massive gains in most stock markets, general sentiment is also showing its very optimistic side again. The indicator has already swung back up from the valley of tears and is now targeting the record level we observed a year ago following the ‘Liberation correction.’ However, this is not a sell signal—any more than it was a year ago. Quite the contrary: it suggests how sustainable the current movement is likely to be, even if things might get a bit bumpy over the next few days as the market consolidates.

As previously discussed, the Strait of Hormuz is not only used for energy exports. The chip and mining industries are also affected. According to the American Farm Bureau Federation (AFBF), around 70% of surveyed U.S. farmers cannot purchase the required amount of fertilizer due to high prices—which is likely to reduce yields next season. The specter of inflation is thus haunting the markets a bit more loudly again, which is why higher interest rates are expected, in turn weighing on the performance of precious metals.

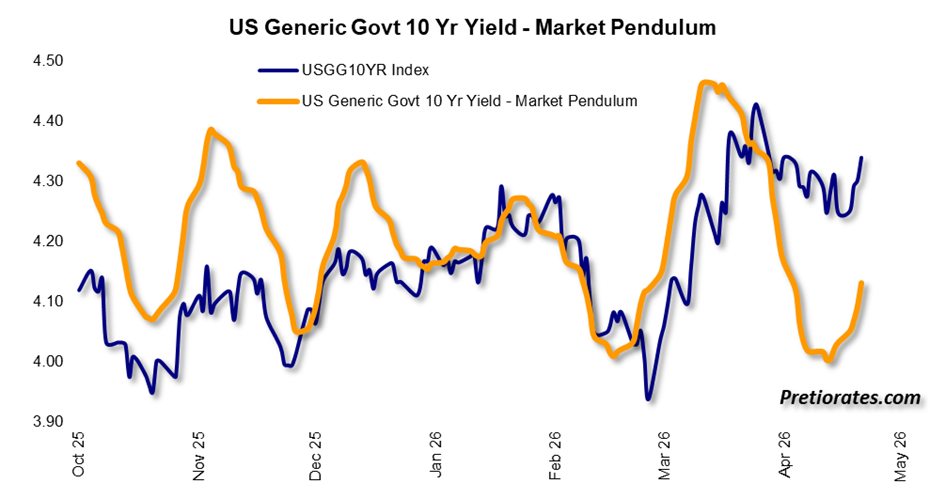

In fact, according to the Market Pendulum, we can expect the market yield on 10-year U.S. Treasuries to continue rising in the coming days and weeks.

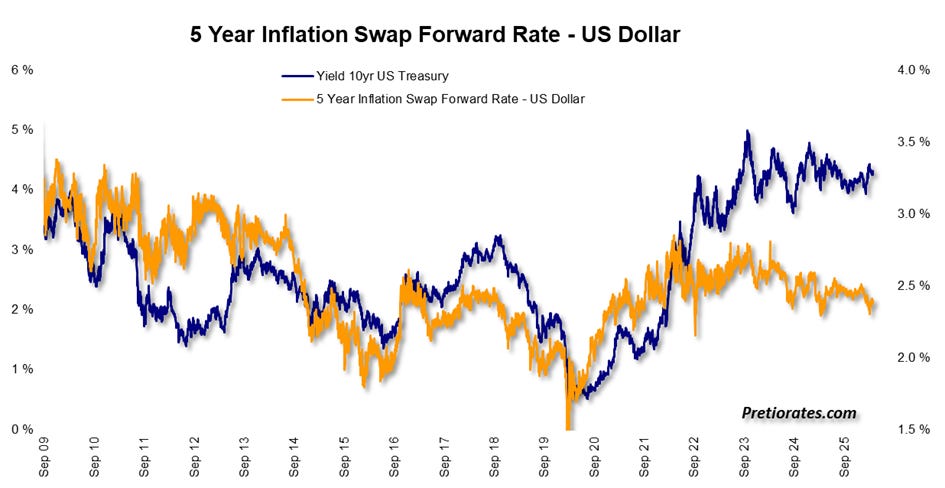

What is intriguing, however, is that U.S. swap markets do not really anticipate higher inflation over the next five years. The swap forward rate over this period remains remarkably subdued.

This is actually the most surprising message from the financial markets over the past week. We are looking into this further, but already recognize the assessment that the selling pressure on precious metals due to potentially higher market interest rates in recent weeks may have been exaggerated. We plan to address this topic next week.

We wish you successful investments!

If you enjoyed this issue, please click on the Like icon at the top or at the bottom of this email. This is very important in helping our Thoughts gain more followers. Thank you!

Yours sincerely,

Pretiorates

Find out more about Pretiorates.com

These thoughts will be available as an AI video on Youtube.com within 48 hours: https://www.youtube.com/@Pretiorates

And don’t forget to recommend us - with the button below.

Remember, we are not making any recommendations for investments, we are just giving you ideas for your own analysis and decisions! Do your own due dilligence!

If you like our short analysis, please recommend us to your friends!

Thank you for being a part of the Pretiorates community. Stay tuned for more updates, analyses, and deep dives into the realms of finance and economics.

Appreciate your anticipation, original tools (graphs). Very useful for yours readers.

Thanks and congrats!

Horacio Costa